Tips for Creating More Privacy in Your New Home

Wednesday, November 4, 2015

So you have just made one of the biggest purchases of your life by buying a home of your own and now you need to make it a bit more private. You have come to the right place! Let’s look at a few tips for creating more privacy in your new home.

- If you happen to live in a big city where the houses are basically on top of each other you may want to line your floors with a lot of area rugs. While this simple step to making more privacy in your new home sounds like a silly thing, it really will help to keep the noise level down to a minimum if your neighbors tend to be loud.

- Lined curtains are a perfect way to help your home feel like an oasis in the middle of the country even if it is not. These types of curtains also help to filter out loud noises as well.

- If you have a spot on your windowsills to put planters they can aid you in making your home more private. All you need to do is put some tall plants in the planters and voila, you will have more privacy from your neighbors.

- One good way to have privacy outdoors for your new home is by putting up a privacy fence. Privacy fences can help to keep pets safe as well as make your outdoor area a nice place to “get away from it all”, which we can all use every now and again.

- Tall scrubs and trees are a great way to shield yourself from your neighbors and make your home feel more private. Scrubs and trees will also help to make your new home more beautiful and help the environment as well.

- If you simply cannot feel enough privacy in your new home, you can hide in a reading nook under the stairs or in a small attic space so that you can escape from time to time from those around you. If your new home doesn’t have a small space like this, you can likely make one quite easily.

Lastly if privacy is extremely important to you, it may be worth your while to look for a home in the wide open country so that you don’t have to make any previsions for more privacy.

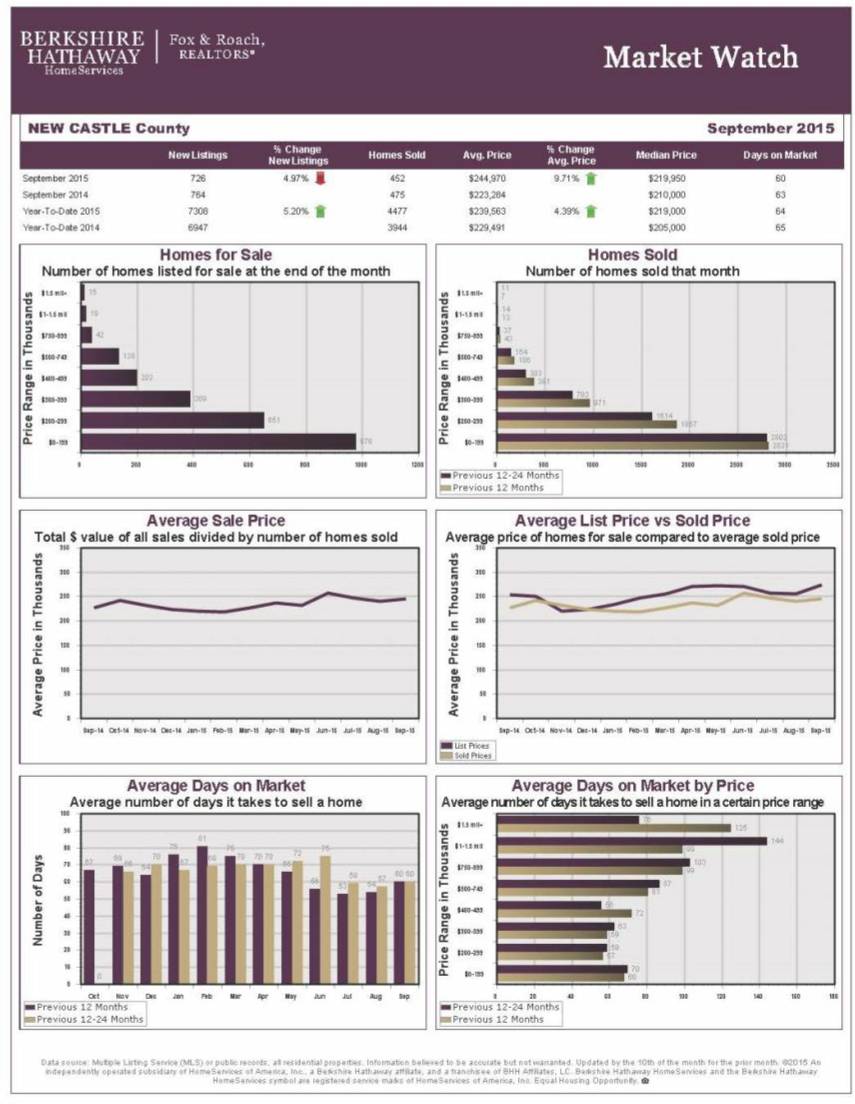

Courtesy of New Castle County DE Realtor Tucker Robbins.

Add Comment